A robo-advisor ofter called a robo-investor is a digital platform that offers automated, technology-driven financial advice and portfolio management. By evaluating users' financial goals, risk tolerance, and preferences through a simple interface, it creates personalized investment strategies. Suitable for both seasoned and novice investors, robo-advisors simplify investing by providing efficient strategies, and broadening access to investment opportunities through continuous optimization and automatic portfolio adjustments.

Whether you're a seasoned investor or a beginner, this overview guides you to the forefront of robo-investing in the UK.

To create this list I had to test these tools one by one and rate them according to their key features like fees and regulatory compliance for efficient wealth management. If you would like to make suggestions for robo advisors that might be missing then feel free to reach me through LinkedIn or by email: george@wealthyhood.com

Quick List of Best Robo Investors for UK Users

Wealthyhood - Best Robo Advisor for Beginners (0 Fees as well)

Nutmeg - Ideal for Tax-Wrapped Investment Strategies

Moneyfarm - Best Robo Advisor Overall

InvestEngine - Best for Low Management Fees

IG Smart Portfolios - Best According to Reviews

Wealthify - Best Because of Minimum Investment

MoneyBox - Best Robo Investor for Micro-Investing

How to Choose a Robo-Advisor?

Selecting the appropriate robo-advisor depends on your investment objectives, experience level, and individual preferences.

I would highly recommend considering the following aspects when evaluating a robo-advisor for your investment needs especially if you are a beginner:

Investment Strategy and Goals Alignment: Ensure the platform aligns with your financial goals and risk tolerance by understanding its investment approach. Ensure you develop a well-thought-out investment strategy before beginning your investment journey.

Fees and Costs: Compare the fees charged by different robo-advisors, including management fees and any additional charges. Always check the fee structure before committing.

Performance History: Research the robo-advisor's track record and performance history to gauge its ability to deliver consistent returns.

Minimum Investment Requirement: Check if the robo-advisor's minimum investment requirement fits your budget and investment capacity.

Range of Assets and Account Types: Evaluate the diversity of investment options and account types offered to ensure they match your preferences and needs. Consider what types of investments the app offers, ranging from stocks and bonds to ETFs and cryptocurrencies.

Customisation and Personalisation: Choose an intuitive and user-friendly investment app that allows for personalised portfolio customisation based on your individual financial situation and objectives.

User Interface and Ease of Use: Opt for an intuitive and user-friendly platform to simplify the investment process. An app's interface should be intuitive and user-friendly, especially for a beginner investor.

Customer Service and Support: Consider the availability and responsiveness of customer support to address any concerns or queries promptly. Reliable customer service is essential, particularly when dealing with financial matters.

Security and Regulation Compliance: Ensure the robo-advisor adheres to industry regulations and employs robust security measures to protect your financial information.

Tax Optimisation Strategies: Select a robo-advisor that incorporates tax optimisation strategies to minimise tax liabilities on your investments.

Withdrawal and Access to Funds: Understand the withdrawal process and ensure it aligns with your liquidity needs and timeline.

Reputation and Reviews: Check for robo-advisors UK reviews and testimonials to gain insights from other users. The stability and dependability of an investment app is a crucial factor to consider. Look for apps that offer strong security measures to protect your personal and financial information.

Note that if you are a more hands-on investor that likes have control over your investments a robo-advisor might not be the best pick for you. You should either be using an investing app for simple investing on the go or use a feature-rich investing platform instead. During my research for Wealthyhood's product I had to go through different competitotors and test in-depth different products to understand the investing market. You can find all my investing tool reviews on my author page.

Now that you know more about how to choose a platform, let’s compare robo-advisors in the UK to help you make an informed decision.

Invest Commission FreeBest Robo Advisors in UK According to Our Research

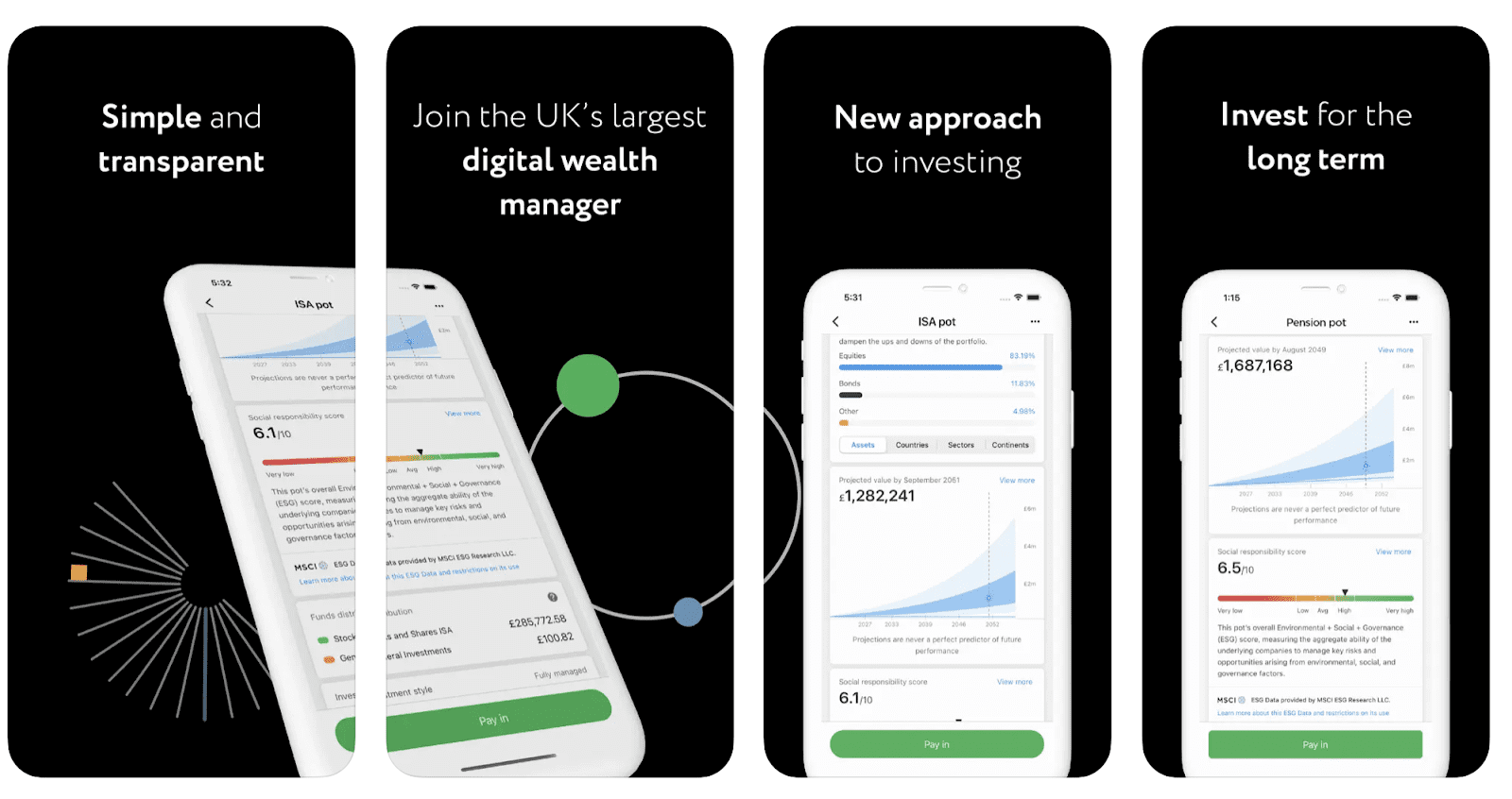

1. WealthyHood - Best Robo Investor For Beginners

WealthyHood provides a convenient and user-friendly investment platform that is ideal for newcomers starting in the financial market. The application has a simple interface designed specifically for novice investors and offers access to a wide range of investment options, including ETFs (exchange-traded funds) and stocks. What is really crazy about Wealthyhood is the fact that the Gold plan offers 4% dividend yield for £12.99/month.

The platform also offers automated portfolio customisation based on individual risk profiles as well as comprehensive training resources for investment knowledge.

Fees: WealthyHood stands out as it offers commision-free investing even in its basic plans. However, certain advanced features may have associated fees, and users should be mindful of potential costs when exploring additional functionalities.

Features: One of WealthyHood's distinguishing features is its support for fractional share investments, allowing users to economically purchase shares in their favourite companies. With a focus on a smooth user experience, the app incorporates various features to streamline the investment process.

Regulatory Compliance and Security: WealthyHood's regulatory status may vary, and users should verify its compliance with relevant authorities. While the platform employs security measures, users should conduct due diligence on regulatory aspects and security protocols.

Pros:

User-friendly interface for beginners

Ready-made portfolio template

Commission-free investing for cost-effectiveness

Unique and engaging experience

Cons:

Commission-free investing is available in paid plans only

WealthyHood’s innovative features cater to investors looking for a modern and collaborative investment experience. Also, WealthyHood stands out from the competition by offering a wide range of training resources to help you better understand the world of finance. Novices will be able to find all the information they need before embarking on their investments.

Try Wealthyhood2. Nutmeg - Ideal for Tax-Wrapped Investment Strategies

I've found Nutmeg to be a robust and user-friendly robo-advisor. Its strength lies in its straightforward approach to investing, which is ideal for beginners or those seeking a hands-off investment experience. Nutmeg's platform offers a variety of portfolio options, including socially responsible and thematic portfolios, allowing for some level of customization based on individual preferences and goals.

The platform's ease of use, both on mobile and desktop, is commendable. Setting up an account is simple, and the range of account types, including ISAs and pensions, caters to various financial needs. However, a notable drawback is the £500 minimum investment requirement, which might be a barrier for those starting with smaller amounts.

Fees: Nutmeg's fee structure ranges from 0.75% to a lower of 0.25%, covering investment management and market spread. While competitive, investors should consider the impact of fees on their overall returns.

Features: Nutmeg's goal-based investing stood out. The platform's intuitive questionnaire tailors portfolios to individual risk preferences, and the diverse range of investment options caters to varied preferences.

Regulatory Compliance and Security: Nutmeg is regulated by the Financial Conduct Authority (FCA), instilling confidence in its regulatory adherence. The platform prioritises data security, employing encryption and secure processes for user protection.

Pros:

User-friendly interface

Commitment to regulatory standards

Automated portfolio management

Transparent fee structure

Cons:

May be limiting for those seeking a hands-on approach

Limited specialised investment options

You should consider the impact of fees on smaller portfolios

Lowest reviews on Trustpilot

Nutmeg impresses with its accessibility, personalised approach, and regulatory compliance. For investors seeking a straightforward robo-advisor with diverse investment options, Nutmeg stands as a solid choice.

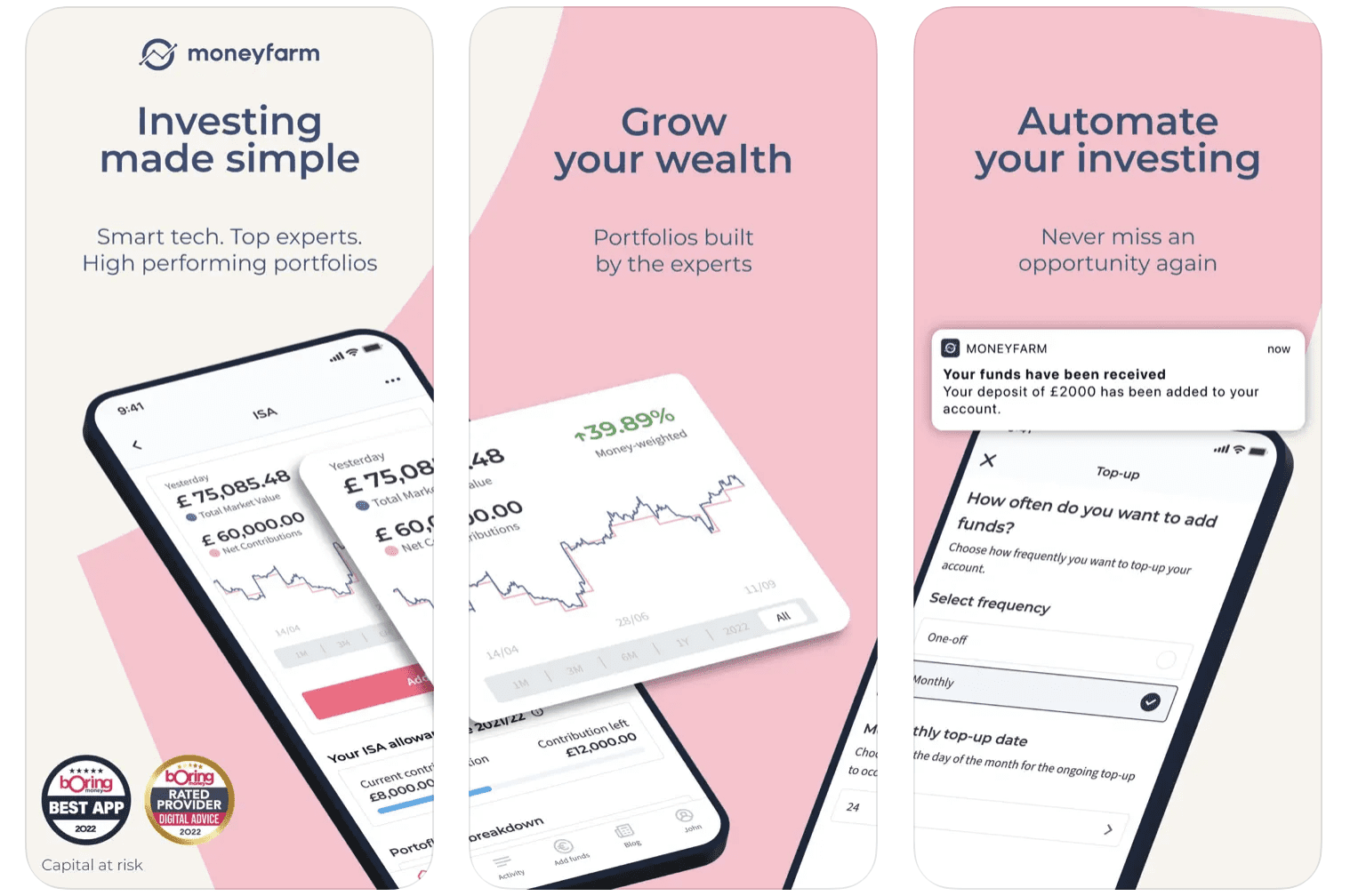

Go to Nutmeg3. Moneyfarm - Best Robo-Advisor Overall

Moneyfarm, is a leading robo-advisor, that offers personalized investment plans akin to traditional financial advisors. It features diverse account types, including Stocks and Shares ISA, General Investment Accounts, and SIPPs, catering to various investment needs. Notable for its low minimum investment requirement and transparent fees, Moneyfarm is accessible to a broad range of investors.

Despite being a robo-advisor, it provides robust human support and continuous portfolio monitoring by experts. Its user-friendly platform and mobile app make investing simple and approachable, while its commitment to customer satisfaction and tax-efficient accounts further enhance its appeal. Moneyfarm is designed to make investing easy and accessible. It offers a straightforward platform where you can set up and manage your investments.

What I appreciate about Moneyfarm is that it takes care of constructing and managing a diversified portfolio on my behalf. It's a cost-effective and efficient option for investing, making it suitable for both beginners and experienced investors alike.

Fees: If you actively manage your portfolio, Moneyfarm's fees are degressive, starting at 0.75% for a minimum amount of £500 and rising to 0.35% (£500,000), with annual fees for investment funds averaging 0.2%. Moneyfarm also offers fixed-allocation portfolios that follow the market without active intervention. Fees are lower, ranging from 0.45% (£500) to 0.25% (£500,000), with an annual fee for investment funds of 0.15%.

Features: Moneyfarm tailors portfolios to individual risk preferences through its objectives-based approach. The app's clear investment strategy and tax-efficient features are highlights, providing a comprehensive investing experience.

Regulatory Compliance and Security: Moneyfarm is regulated by the Financial Conduct Authority (FCA), instilling confidence in its regulatory adherence. The platform prioritises data security through encryption, contributing to a robust and safe investment environment.

Pros:

User-friendly design

Goal-oriented investing

Commitment to FCA regulations

Tax-efficient features

Cons:

A restricted selection of portfolios is offered

Not the best option for experienced investors

High platform fee for smaller portfolios

High fund fees on classic portfolio

Moneyfarm offers a streamlined robo-advisor experience with a strong emphasis on user simplicity and goal-based investing. I wouldn’t recommend this robo-investor tool to someone who cares about the fees though.

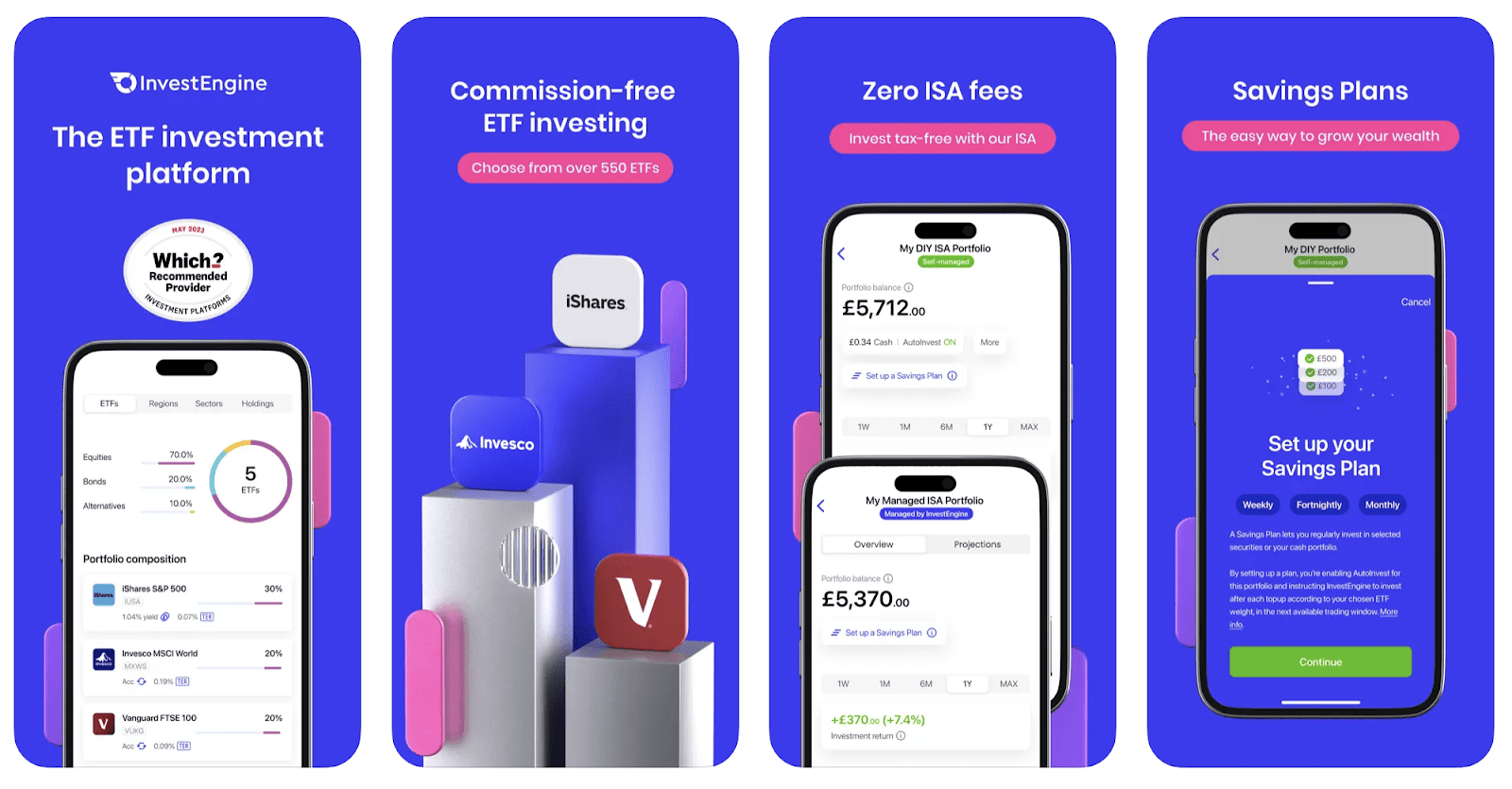

Go to Moneyfarm4. InvestEngine - Best Because of Low Management Fee

During my testing, I found out that InvestEngine offers a straightforward and cost-effective solution for both DIY and managed investing. Its focus on ETFs and absence of direct stock market trading suit those looking for a simplified investment approach. The platform's low fees are a major draw, especially for beginners or those looking to keep costs down. Although the range of ETFs may seem restrictive to some, the ease of use and efficient customer support make it a viable option for those new to investing or preferring a more hands-off approach. Overall, InvestEngine strikes a good balance between simplicity, affordability, and choice.

Fees: InvestEngine operates with a transparent fee structure, with an annual management fee of 0.25%. This competitive pricing adds to the platform's appeal, especially for investors conscious of minimising costs.

Features: InvestEngine's broad range of diversified portfolios cater to various risk preferences and investment goals. The platform's automatic rebalancing and tax-efficient strategies contribute to a hands-off and efficient investment journey.

Regulatory Compliance and Security: InvestEngine adheres to the regulatory standards set by the Financial Conduct Authority (FCA), ensuring a secure and compliant investment environment. The platform employs robust security measures, including encryption, bolstering the safety of user data.

Pros:

Low-cost structure

Diversified portfolios

Tax-efficient features

Straightforward approach to investing

FCA regulation for reliability

Cons:

No income portfolio

Lack of phone support

Competitive fees but limited investment options

Simplicity may be limiting for users seeking advanced features

Overall, InvestEngine provides a user-friendly and cost-effective robo-advisor solution. With competitive fees, a variety of portfolios, and robust security measures, it's a strong choice for investors seeking simplicity and reliability in their investment journey.

Go to Invest Engine5. IG Smart Portfolios - Best According to Reviews

IG Smart Portfolios is one of my favorite robo-investors, as it offers an automated and professional approach to investing. With user-friendly features and a solid foundation, IG Smart Portfolios provides a smooth way for investors to access diversified portfolios aligning with their financial goals.

Fees: The IG Smart portfolio offers a clear pricing structure with management fees at 0.50% and capped at £250 per year per account type. Portfolios with a value over £50,000 do not pay management fees, only the average fund cost of 0.13% and transaction cost of 0.09%.

Features: You can anticipate a range of features, from automated portfolio management to diversified investment options. The platform's customisation tools and risk assessment mechanisms contribute to a tailored investment experience.

Regulatory Compliance and Security: IG Smart Portfolios adheres to regulatory standards, providing investors with a level of confidence in the platform's reliability and security.

Pros:

User-friendly interface

Educational resources for novice and experienced investors

Cons:

The range of investment options may be narrower

Importance of understanding the fee structure in detail

Potential for surprises, necessitating careful assessment of overall cost-effectiveness

In summary, IG Smart Portfolios offers a straightforward robo-investment experience with user-friendly features and transparent fees. While it emphasises regulatory compliance, it has some limitations, including a narrower range of investment options and the need for careful consideration of the fee structure for cost-effectiveness.

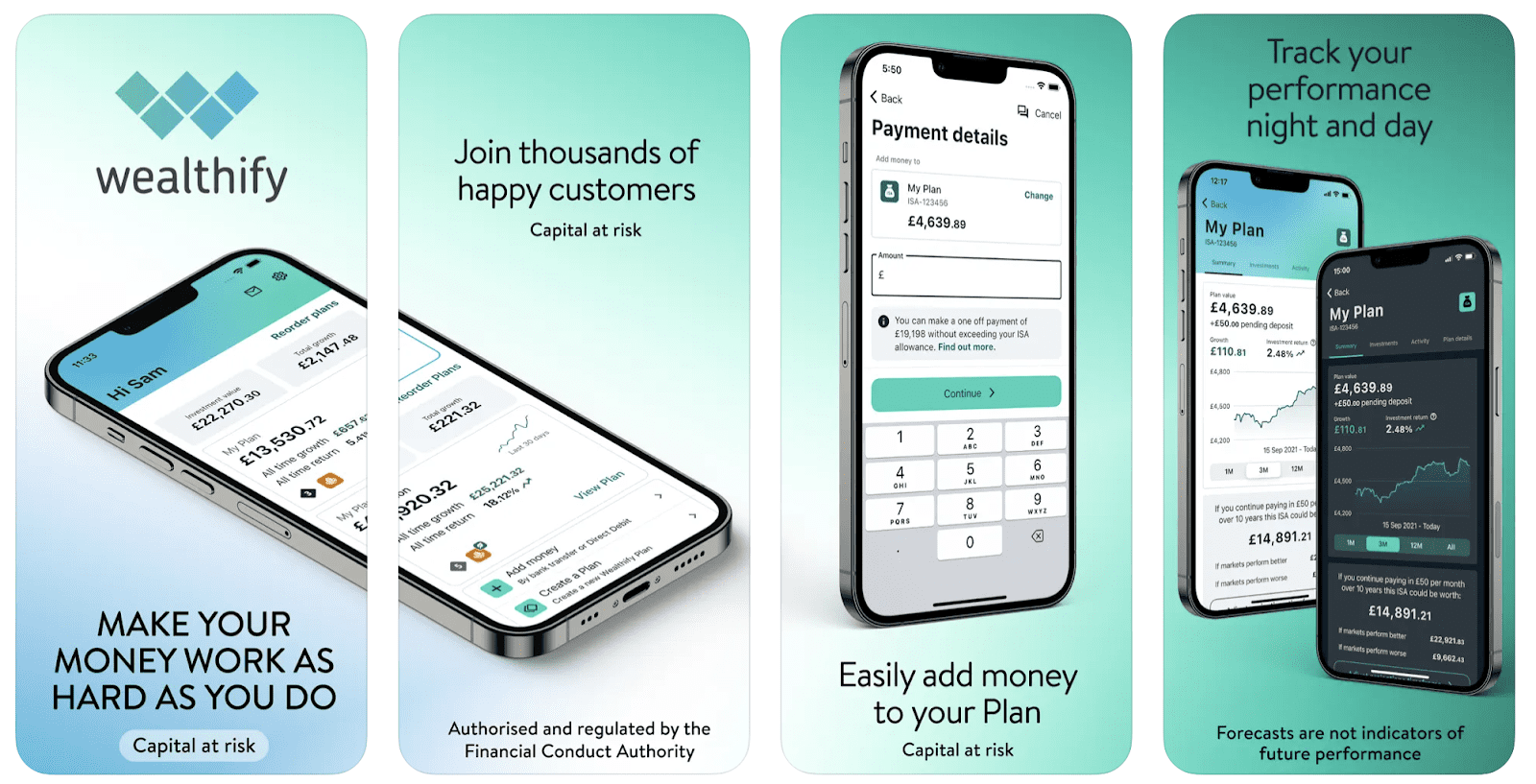

Go to IG6. Wealthify - Best Because of Minimum Investment

Wealthify aims to make investing straightforward and accessible. It provides a user-friendly platform where you can easily set up and manage your investments. With Wealthify, you don't need to be a financial whizz.

The process of setting up an account and selecting investment options is easy to navigate.

What I loved about Wealthify is their approach, which involves experts handling the investment process, is ideal for individuals who prefer not to delve into the intricacies of investment decision-making.

Fees: Wealthify offers an annual fee of 0.6% without any additional charge for depositing, withdrawing, transferring, or closing your plan. However, additional charges may apply (e.g. fund charges taken directly by the fund provider), which Wealthify aims to keep as low as possible (around 0.16% for original plans and 0.7% for ethical plans).

Features: Its diverse range of investment options and the ability to customise portfolios based on individual risk preferences. The platform's goal-based investing and ethical investment options are particularly noteworthy.

Regulatory Compliance and Security: Wealthify is regulated by the Financial Conduct Authority (FCA), providing a sense of security for users. The platform prioritises data encryption and secure processes, enhancing overall safety.

Pros:

User-friendly interface

Goal-based investing

Ethical investment choices

FCA regulation for added trust

Strong commitment to security

Cons:

Competitive but noteworthy fees

Diverse but not the most extensive range of assets

Overall, Wealthify stands out for its accessible design, ethical investment options, and regulatory compliance. While fees may be a factor, its overall user experience and commitment to security make it a compelling choice for investors seeking a balanced and intuitive robo-advisor.

Go to Wealthify7. Moneybox - Best Robo-Advisor for Micro-Investing

Based on my experience with Moneybox, it's a solid choice for someone looking for a hassle-free investment approach. The platform, designed as a robo-advisor, effectively takes on the role of a financial advisor, crafting a personalized investment strategy based on an individual's risk profile. This automation in portfolio management is particularly reassuring, as it eliminates the potential biases often seen with human financial advisors.

Moneyfarm's investment portfolios, primarily composed of ETFs, are tailored according to your risk tolerance and are regularly adjusted to suit market conditions and personal circumstances. This approach to investment is both efficient and practical, especially for those who may not have the time or expertise to manage their investments actively.

However I found my small testing portfolio eroding due to the high so this is something to consider if you are investing with £1000 or less.

Fees: For its various investment accounts, including the Stocks & Shares ISA, the General Investment Account, and the Stocks & Shares Lifetime ISA, Moneybox implements a simplified fee structure with a fixed monthly subscription of £1. In addition, an annual platform fee of 0.45%, calculated daily and charged monthly based on the value of the investment, is also levied when selling the largest holding.

Features: Moneybox's round-up feature effortlessly investing spare change from daily transactions. The platform also offers a variety of themed investment options, catering to different preferences and the ability to set recurring investments.

Regulatory Compliance and Security: Moneybox is regulated by the Financial Conduct Authority (FCA), ensuring adherence to regulatory standards. The platform employs robust security measures, including data encryption, to safeguard user information and investments.

Pros:

Micro-investing approach

Round-up feature for accessibility

Themed investment options for personalisation

FCA regulation for trust

Cons:

Fees can become relatively high for larger portfolios

Simplicity may limit advanced features

May not offer the breadth of investment options for experienced investors

Moneybox makes investing approachable, especially for beginners. While the fees are reasonable for small investments, consider your long-term goals and preferences when evaluating this user-friendly platform.

Go to MoneyboxWhat is The Cheapest Robo-Advisors in UK?

Here’s a list of the cheapest robo-advisors in the UK, according to the fees.

Moneyfarm

Fees: Moneyfarm's fees vary between 0.25% and 0.75% per year. The exact fee depends on the amount invested, with higher investments typically attracting lower percentage fees.

Cost-Related Features

Tiered Fee Structure: The more you invest, the lower the percentage fee you pay.

Additional Costs: Besides the annual management fee, investors should also consider underlying fund charges, which are additional but generally low due to the use of ETFs.

No Transaction Fees: Moneyfarm does not charge fees for transactions, including buying and selling of investments within the portfolios.

Wealthify

Fees: Wealthify charges a flat annual fee of 0.60%, regardless of the investment amount.

Cost-Related Features

No Minimum Investment: Allows investments from as low as £1, making it highly accessible.

Transparent Pricing: The flat fee structure makes it easy for investors to understand and calculate their costs.

Underlying Fund Charges: Investors should also account for the costs of the underlying funds, which can vary based on the chosen portfolio.

Nutmeg

Fees: Nutmeg's fees range from 0.25% to 0.75% per year, depending on the chosen investment style and portfolio size.

Cost-Related Features

Tiered Pricing Model: Similar to Moneyfarm, Nutmeg offers a tiered fee structure, where the fee percentage decreases as the investment amount increases.

Fund Costs: Includes additional costs for the underlying investments, typically ETFs, which are relatively low.

No Exit Fees: Nutmeg does not charge fees for withdrawing funds or closing the account.

Wealthyhood

Fees: Wealthyhood has a fair fee structure and it also eliminates the order and transaction fees in the paid plans. Plans are available on their pricing page.

Cost-Related Features

Low-Cost Investment Options: Typically, robo-advisors like Wealthyhood use ETFs and index funds, which have lower management fees compared to actively managed funds.

Potential for Low or No Minimum Investment: Many robo-advisors allow investors to start with very low or no minimum investment, increasing accessibility.

Automated Portfolio Management: This feature usually reduces the need for costly human advisors, passing on the savings to the investor.

General Cost Considerations for Robo Investors:

Annual Management Fees: This is usually a percentage of the invested assets and varies between providers.

Underlying Fund Charges: Additional costs associated with the ETFs or mutual funds used in the portfolios.

Transaction Fees: Some robo-advisors may charge for transactions within the portfolio, though this is less common.

Minimum Investment Requirements: Can influence the accessibility of the service for investors with limited capital.

Tiered Pricing Structures: Often, the more you invest, the lower the percentage fee you pay.

When choosing a robo-investor, it's crucial to consider both the explicit fees and the potential hidden costs, like the underlying fund charges, to understand the total cost of the investment service.

What is A Robo-Advisor?

A robo-advisor is a digital platform and automatic investing app that uses algorithms to automate investing with little human intervention. It collects information about a client's financial situation and goals through an online survey. Then, it uses this data to create and manage a diversified investment portfolio, considering factors like risk tolerance, investment goals, and market conditions.

Unlike typical investing apps, robo-advisors offer personalised investment strategies and automatically adjust portfolios for optimal asset allocation and tax efficiency. They're cost-effective and provide ongoing management, making them a great tool for investors seeking a systematic and automated approach to wealth management.

How Do Robo Advisors Work?

Robo advisors work by using sophisticated algorithms to provide automated investment management services. Initially, they gather information from clients through a questionnaire to assess their financial situation, investment goals, and risk tolerance. Based on these inputs, the robo advisor algorithm constructs a personalized investment portfolio, often utilizing a mix of exchange-traded funds (ETFs) to ensure diversification across different asset classes. The portfolios are typically designed following modern portfolio theory principles, aiming to optimize returns for a given level of risk. Robo advisors also handle ongoing portfolio management tasks, such as rebalancing and tax-loss harvesting, to maintain the portfolio's target asset allocation and enhance tax efficiency. This automated process makes robo advisors a cost-effective and efficient option for individuals seeking a passive investment approach. Here is a step-by-step of a typical Robo Advisor user onboarding process.

User Onboarding:

You fill out an online questionnaire, providing details about your financial goals, investment horizon, income, and risk tolerance.

Profile Analysis:

The robo advisor analyzes your responses to determine an appropriate investment strategy tailored to your profile.

Portfolio Construction:

Utilizing algorithms, it builds a diversified investment portfolio, typically comprising a mix of ETFs across various asset classes.

Automated Investing:

Your funds are automatically invested in the chosen portfolio.

Continuous Monitoring:

The robo advisor monitors market conditions and portfolio performance.

Portfolio Rebalancing:

Periodic adjustments are made to maintain the desired asset allocation and manage risk.

Tax Optimization (if applicable):

Strategies like tax-loss harvesting are employed to optimize tax efficiency.

Reporting and Access:

You receive regular updates and have online access to track your portfolio’s performance.

Adjustments Based on Life Changes:

You can update your profile for any significant financial or personal changes, prompting the robo advisor to adjust your investment strategy accordingly.

Do Robo-Advisors Beat the Market?

The performance of robo-advisors in beating the market varies. Some robo-advisors have demonstrated competitive returns, while others may not consistently outperform market benchmarks like the S&P 500.

It's essential to consider factors such as investment strategy, market conditions, and individual risk preferences. Studies, such as the Robo Report by Backend Benchmarking and comparisons by financial platforms like NerdWallet, provide insights into the performance of specific robo-advisors.

While robo-advisors may not consistently outperform the market, they can offer a cost-effective and efficient way for investors to gain exposure to diversified portfolios tailored to their risk preferences.

Robo-Advisors Over ETFs?

Robo-advisors and ETFs (Exchange-Traded Funds) are both popular investment choices, but they serve different roles in a portfolio. Robo-advisors are automated platforms that use algorithms to create and manage diversified portfolios tailored to individual investors. ETFs, however, are investment funds traded on the stock market, giving investors access to a diversified portfolio of assets.

When comparing robo-advisors and ETFs, factors like cost, diversification, and user-friendliness are often considered. Here's a quick breakdown:

Diversification:

Robo-advisors are designed to provide automatic diversification by allocating investments across a mix of asset classes based on an investor's risk tolerance and financial goals.

ETFs inherently offer diversification by tracking an index or a specific sector, allowing investors to gain exposure to a broad range of assets in a single investment.

Cost:

Robo-advisors typically charge a management fee, which can range from 0.25% to 0.75% of the assets under management. This fee covers the automated management of the portfolio.

ETFs generally have lower expense ratios compared to traditional mutual funds, making them cost-effective for passive investors. However, investors may still incur trading commissions when buying or selling ETFs.

Ease of Use:

Robo-advisors are known for their user-friendly interfaces and automated features, making them accessible to both novice and experienced investors.

ETFs can be bought and sold like individual stocks on the stock exchange, requiring investors to place trades through a brokerage platform.

Expected ROI for Robo-Advisors: Understanding the Key Influencers

The typical annual return for robo-advisors can vary widely, often ranging between 2% to 8%, depending on market conditions and the investment strategy employed. However, this is a general estimate and actual returns can differ based on the specific robo-advisor and the individual investor's portfolio choices.

The Return on Investment (ROI) for a robo-advisor varies based on several factors. Key influencers include:

Risk Tolerance

Conservative Portfolios: Lower risk, typically lower ROI. Suitable for risk-averse investors.

Aggressive Portfolios: Higher risk, potentially higher ROI. Preferred by those who can tolerate market volatility.

Investment Strategy

The strategy, especially the asset allocation and diversification across asset classes (stocks, bonds, etc.), influences returns.

Robo-advisors use algorithms to maintain a portfolio that balances performance with the investor's goals and risk profile.

Market Conditions

Economic factors, interest rates, and global events can significantly impact the markets and, consequently, the ROI.

Market conditions are unpredictable, making ROI subject to fluctuations.

Robo-Advisors and Risk Management

Robo-advisors are designed to provide competitive returns by leveraging diversification and implementing automated rebalancing strategies to manage investment risks.

Historical performance data can offer valuable insights into how investments might perform, but it's crucial to understand that this data is not indicative of future results. Investors should not view past performance as a guarantee for future ROI.

For investors, it's essential to align their investment expectations with their financial goals and risk tolerance levels. They should also be cognizant of the unpredictability inherent in market conditions and how this can impact investments managed by robo-advisors. In this context, consulting a financial advisor can be highly beneficial for obtaining personalized investment advice.

Important Note

Remember, while robo-advisors provide an efficient investment management solution, the actual ROI is influenced by personal and market-related factors, and there are no guaranteed returns.

For more detailed insights on investment strategies and risk management with robo-advisors, you might find these resource helpful:

Understanding these aspects can help you make informed decisions about using robo-advisors for your investment needs.

How Risky Are Robo Investors? Can You Lose Money?

Investment Performance and Market Fluctuations: Like any investment, robo advisors are subject to market risks. They typically invest in exchange-traded funds (ETFs), which means the value of their investments can rise and fall with market conditions. Market volatility is a significant factor, and there's no immunity against investment losses with robo advisors.

Algorithmic Decisions and Portfolio Management: Robo advisors use algorithms to determine your risk profile and manage your investments accordingly. However, not all algorithms are equally effective. Some may create more volatile portfolios, leading to higher risks in the short term. If a robo advisor fails to manage the portfolio effectively or takes on excessive risk for higher returns, it could result in financial losses.

Asset Allocation: One of the critical functions of robo advisors is allocating assets based on your risk tolerance. However, if the algorithm doesn't accurately match your risk profile, it could lead to inappropriate asset allocation. For example, holding a larger number of equities than bonds in a bear market could significantly reduce the value of your portfolio.

Fees and Charges: While robo advisors generally offer low management fees, there is a range in what they charge - from 0% up to 1% of the assets under management. Higher fees could potentially erode your investment returns over time, especially if they don't correspond to better performance or additional services like access to human financial advisors.

Poorly Managed Portfolio: A robo advisor's performance is also gauged by its ability to manage risk and prevent losses. If a robo advisor engages in aggressive trading or makes bad investment calls, it could lead to significant losses. Thus, even with automated management, the possibility of a poorly managed portfolio cannot be entirely ruled out.

Investing with robo advisors carries inherent risks, similar to other investment forms. Understanding these risks and how they align with your financial goals and risk tolerance is crucial. While robo advisors offer a convenient and often cost-effective way to invest, particularly for those with limited time or expertise, they are not foolproof. Thorough research and possibly consulting with a financial professional could be wise steps before committing to a robo advisor for your investment needs.

Are Robo Advisors Better Than Financial Advisors?

Deciding whether robo-advisors are better than financial advisors depends largely on individual needs and preferences. Robo advisors offer automated, low-cost investment services, making them ideal for those seeking simplicity, affordability, and a hands-off approach. They're particularly beneficial for investors with straightforward financial goals and a great alternative to investing apps for beginner investors.

On the other hand, traditional financial advisors provide personalized guidance, and tailored strategies, and can address complex financial situations involving estate planning, tax strategies, or retirement planning. They offer a human touch that's invaluable for investors who prefer direct interaction and customized advice. Ultimately, the choice hinges on the level of customization, cost, and personal interaction you prefer in managing your investments.

Key Takeaways

In concluding our exploration of the best robo-advisors in the UK, we have evaluated these platforms, striving for objectivity and transparency. Our commitment is to empower readers with accurate information for well-informed investment decisions.

These robo-advisors, with features ranging from tax-efficient portfolios to user-friendly interfaces, are reshaping the landscape of wealth management in the UK. However, it's imperative to recognise that investing inherently carries risks, and past performance is not indicative of future results. We advocate for thorough research and a clear understanding of your risk tolerance before making investment decisions.

Should you have any inquiries or seek further clarification, don't hesitate to engage with me through comments or reach out on social media. I am always reachable through email or even through my personal LinkedIn.

Your financial journey deserves the utmost attention and knowledge. Wishing you happy and informed investing!

Join the Investors' Club

Get access to professional investing tools for free and start building your wealth today!

Capital at risk